Who Leads Public Audits in West Michigan? The Trends in Age, Education, and Diversity of Local Audit Engagement Partners

By Sarah Cole, M.S.A Candidate

Nicole Hafner, M.S.A. Candidate

Emily Voisinet, M.S.A. Candidate

Chenyong Liu, Ph.D., Assistant Professor, School of Accounting

As leaders take the ultimate responsibility for financial assurance engagements, audit partners significantly impact their clients’ financial reporting quality and tax behaviors, which are critical to the growth of the local economy (Lee et al., 2019). Following a descriptive study model, this paper summarizes the general information of West Michigan audit leaders during the most recent 10 years.

Specifically, with the full audit partner name list obtained from the Public Company Accounting Oversight Board (PCAOB), among the 98 Michigan audit partners signed audit reports for publicly traded firms during 2016 – 2025, we identified the 18 who were based in West Michigan. Based on information manually collected from public resources (e.g., social media), our analyses show that audit partners in West Michigan: 1) are 52 years old on average, 2) 54% hold degree(s) from local universities/colleges, and 3) about 72% are perceived as male based on their names and pronouns listed on professional profiles.[1]

Ages of Audit Partners in West Michigan

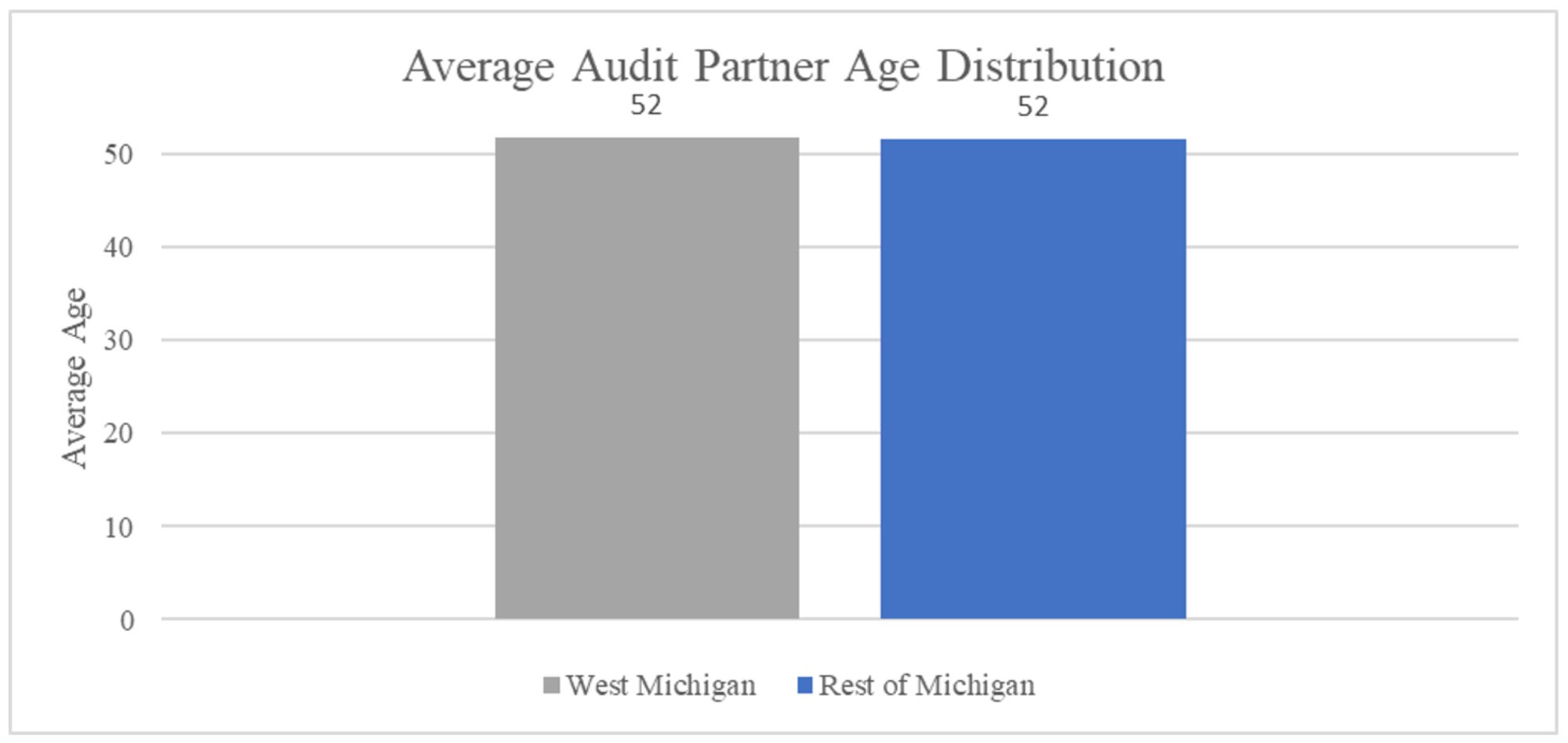

Figure 1 below highlights the average audit partner age in West Michigan compared to the rest of the state; both have an average audit partner age of 52.

Figure 1: Average Audit Partner Age in West Michigan and the Rest of Michigan

Description: The bar chart above shows that the average age of audit partners for public firms is the same in West Michigan compared to the rest of the state. West Michigan audit partners included in this figure are mainly the residents of Grand Rapids, Hudsonville, and Rockford. Two observations were excluded from the rest of Michigan calculation due to public records not being available.

Source: Publicly available information from accounting firms’ webpages and social media such as LinkedIn.

Because audit partners usually retire at 55-62 years old (Cohn, 2021), West Michigan’s current average audit partner age indicates more opportunities for younger auditors in the next five to ten years. According to the statistics from censusreporter.org, West Michigan residents’ average age is 39.8, meaning that the local talent pool continues to fulfill the need for future audit leaders, but it will take the educational institutions in West Michigan to prepare young professionals for this role.

Educational Background of Audit Partners in West Michigan

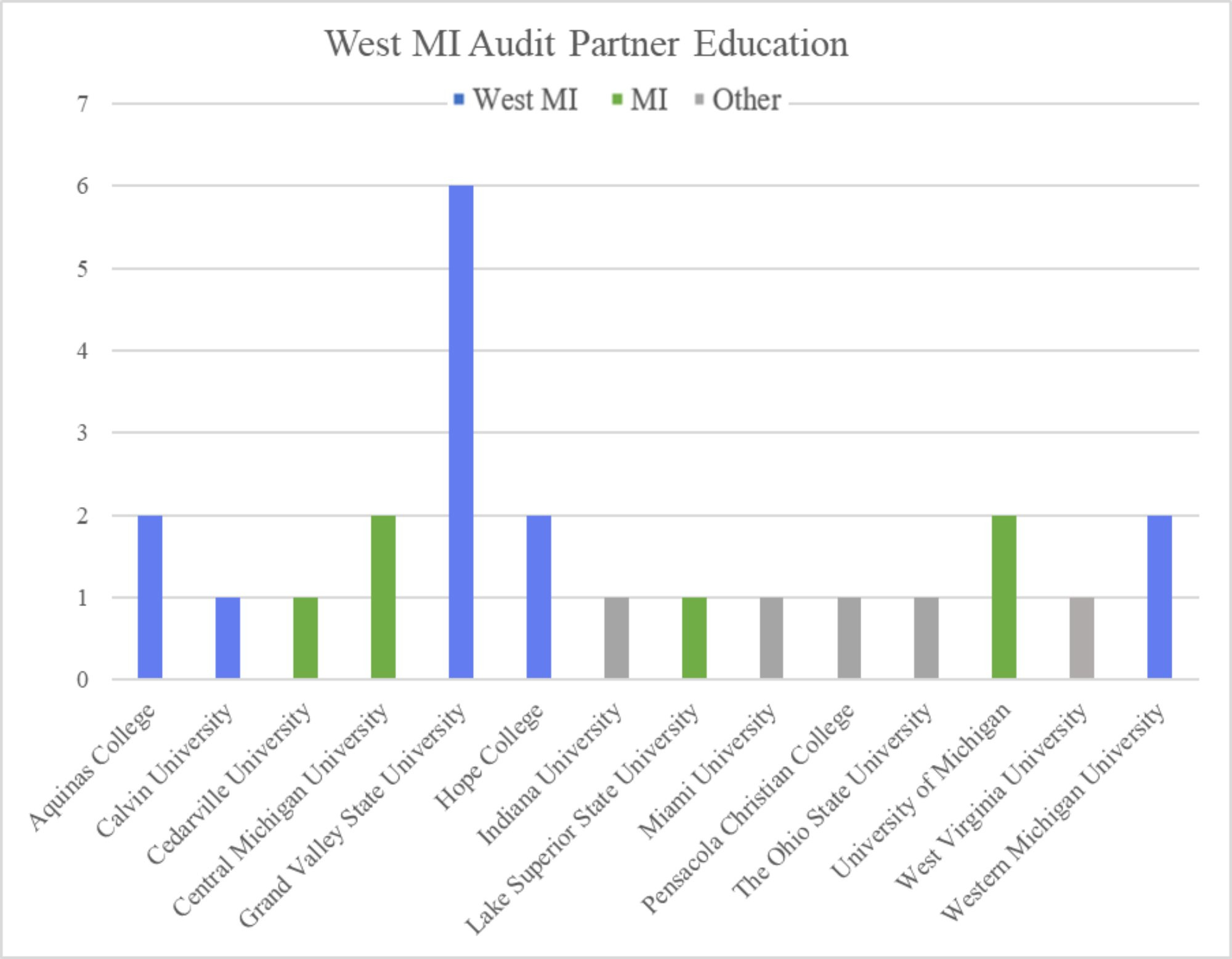

Figure 2 below shows the array of college institutions that West Michigan audit partners attended. Highlighted in the legend is the relative location of each college, indicating if its location is in West Michigan, the rest of Michigan, or other states.

Figure 2: Colleges of West Michigan Audit Partners Attended

Description: The bar chart provides information on the colleges attended by Michigan (i.e., MI) and West Michigan (i.e., West MI) audit partners. The colleges/universities included in “West MI” are Aquinas College, Calvin University, Grand Valley State University, Hope College, and Western Michigan University. Because college-level education includes primary (i.e., bachelor’s) and secondary (i.e., postgraduate) degrees, the 18 West MI audit partners in total hold degrees from 23 different institutions.

Source: Publicly available information from accounting firms’ webpages and social media such as LinkedIn.

Most West Michigan audit partners’ degrees are from Grand Valley State University. This demonstrates the university’s influence in West Michigan and its proximity to the city of Grand Rapids where large audit firms have offices, indicating strong connections between local universities and employers.

As of 2025, West Michigan is home to at least ten colleges and universities, with Grand Valley State University and Western Michigan University as the fourth and fifth largest universities in the state based on enrollment (CollegeSimply, 2025). The theory of the Gravity Model of Migration (GMM) suggests that graduates often remain near their universities after graduation; hence, among the valuable experiences that local colleges and universities provide, new and bright individuals are important to the sustainability of West Michigan businesses, highlighting the necessity of continuing support to educational resources in the region.

Table 1: Audit Partners’ Postgraduate Degree Achievement

Description: The table above shows audit partners’ residence location in the left column and the percentage of partners who earned a postgraduate degree in the right column. A postgraduate degree among our sample of audit leaders mainly includes Master of Business Administration (MBA), Master of Science in Accounting (MSA), and Master of Accountancy (MAcc) degrees.

Source: Publicly available information from accounting firms’ webpages and social media such as LinkedIn.

The data we collected in Table 1 illustrates that a higher percentage of audit partners in West Michigan have earned a secondary degree compared to those in Michigan as a whole. This could indicate a higher level of investment in education in West Michigan, especially for those who were targeting accounting/auditing jobs in the local area.

Perceived Gender Diversity of Audit Partners in West Michigan

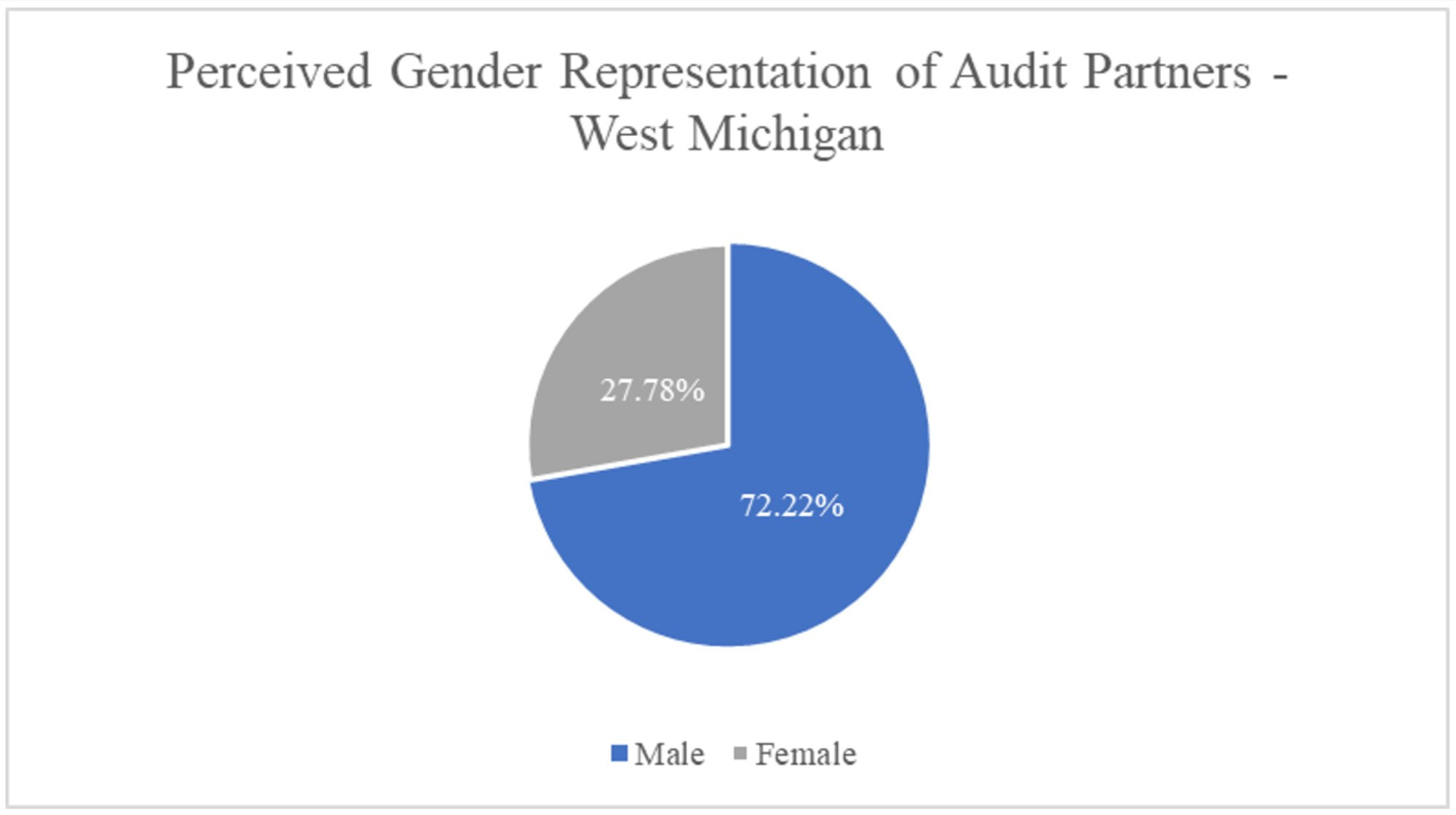

Figure 3 below demonstrates the perceived gender distribution of West Michigan audit partners responsible for public firm audit reports. The data revealed a significant gender presentation imbalance, with 72.22% of the audit engagement partners perceived as male and 27.78% perceived as female based on publicly available information.

Figure 3: Perceived Gender Distribution of Audit Partners in West Michigan

Description: Figure 3 illustrates a pie chart noting percentages of perceived gender representation of audit partners who signed public firms’ audit reports during 2016-2025 in West Michigan. These audit partners are mainly based in Grand Rapids, Hudsonville, and Rockford.

Source: Publicly available information from accounting firms’ webpages and social media such as LinkedIn and X (formerly known as Twitter).

Consistent with the findings in prior literature (e.g., Peters, 2023), the typically male leaning gender representation among audit partners is evident in the West Michigan region. We acknowledge that these binary terms cannot fully represent all gender identities, although perceived males dominate in obtaining audit leadership positions.

Table 2 below shows the breakdown of perceived gender composition of audit partners across Michigan, separating West Michigan from the rest of the state.

Table 2: Perceived Gender Composition of All Michigan Audit Partners

Description: Table 2 presents the perceived gender composition of all the audit partners across Michigan, specifically comparing West Michigan (first column) to the rest of the state (second column).

Source: Publicly available information from accounting firms’ webpages, Form AP dataset provided by the PCAOB, and social media such as LinkedIn.

The comparison in Table 2 postulates that a perceived gender imbalance remains apparent even at the state level. The finding suggests that gender diversity may be more limited in West Michigan compared to the rest of the state. Possible reasons for this observation include unequal access to mentorship or implicit biases in promotion; therefore, there is clearly room for targeted initiatives that aim to diminish the possible gender imbalance among audit partners statewide.

Conclusion

This paper presents evidence that highlights some important dynamics shaping the future of the audit profession in West Michigan. First, the age distribution of current audit engagement partners in the area suggests a possible transition in leadership within the next decade. As a sizable proportion of partners approach traditional retirement age, the demand for qualified successors will increase, providing more opportunities for younger auditors.

Second, the strong representation of local universities shows the critical role that West Michigan’s higher-education institutions play in supplying the audit talent pipeline. Consistent with the Gravity Model of Migration, our analysis confirms that many audit leaders remain in the region after receiving their education in West Michigan, suggesting that ongoing investment in accounting programs is closely tied to sustaining the local professional services ecosystem.

Third, the perceived gender imbalance observed in both West Michigan and the broader state reflects a continuing challenge for the profession as prior research shows that females remain underrepresented in audit leadership roles despite entering the profession at similar or higher rates than males (Didia and Flasher, 2021). For West Michigan accounting firms, we suggest stronger mentorship programs to benefit all employees, equitable promotion processes, and deliberate efforts to support diversity in the leadership pipeline.

Overall, the results in this article point to both opportunities and areas requiring attention. With strong educational institutions and an incoming wave of leadership turnover, West Michigan is positioned to develop the next generation of audit engagement partners for public firms. However, achieving this potential will require coordinated efforts among universities, employers, and community stakeholders to build an inclusive and sustainable audit workforce.

Notes

[1] The analysis is based on the information from public sources such as social media, the PCAOB official website, and corporate webpages. We report the gender presentation in binary terms (male/female) to align with the available data, although we acknowledge that the dichotomy presentation oversimplifies the diversity of gender identities.

References

Cohn, M. (2021). Older auditors are being forced out at firms despite pulling in bigger fees. Accountingtoday.com, N.PAG.

CollegeSimply. (2025). Colleges with the Largest Enrollment in Michigan. CollegeSimply. https://www.collegesimply.com/colleges/rank/colleges/largest-enrollment/state/michigan/

Didia, L. N., & Flasher, R. (2021). Beyond the top seven firms: Gender diversity of audit firm partners and their undergraduate accounting faculty. Journal of Accounting Education, 56, 100739.

Lee, H. S., Nagy, A. L., & Zimmerman, A. B. (2019). Audit partner assignments and audit quality in the United States. The Accounting Review, 94(2), 297-323

Peters, S. J. (2023). The Audit Gender Gap: Has It Narrowed. CFA Institute.

Chenyong Liu, Ph.D., Assistant Professor, School of Accounting